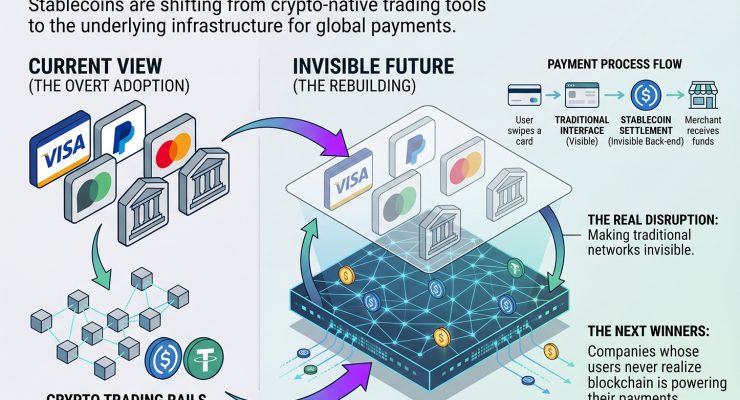

The real disruption in digital payments is not that stablecoins are challenging banks. It is that banks are rebuilding themselves on top of stablecoins and doing so quietly enough that their customers will never notice. Visa, PayPal, and Stripe have not abandoned traditional payment infrastructure; they are using stablecoins to replace the parts of it that are slow, expensive, and invisible to consumers. The winners of the next financial decade may not be the companies that loudly adopt crypto, but the ones whose users never realise blockchain is powering their transactions.

Traditional Finance Is Not Fighting Stablecoins It Is Building on Them

For most of the past decade, the narrative around stablecoins and traditional finance was adversarial. Incumbent institutions warned of systemic risk; regulators circled the space; banks treated blockchain as a threat to be managed rather than a technology to be used.

That narrative has quietly collapsed. PayPal launched its own dollar-pegged stablecoin, PYUSD, in August 2023, becoming the first major payments company to issue a proprietary digital dollar. Visa has partnered with Circle to settle transactions in USDC across Ethereum and Solana removing the need for traditional correspondent banking in cross-border settlement. Stripe, which exited crypto payments in 2018, reversed course in 2024, citing stablecoin maturity as the primary reason. JPMorgan has run its own blockchain-based settlement network, Onyx, since 2020, processing interbank transactions that never touch a public blockchain but use the same architectural logic. These are not pilots. They are production infrastructure.

Why Stablecoin Payment Infrastructure Works Where Other Crypto Did Not

Bitcoin and Ethereum failed as everyday payment systems for a straightforward reason: their values move too much. A token that trades at $60,000 one week and $30,000 six weeks later is a speculative asset, not a medium of exchange. Neither merchants nor consumers can price, plan, or account in something that volatile.

Stablecoins sidestep that problem by design. Pegged 1:1 to fiat currencies overwhelmingly the US dollar they retain the stability of traditional money while inheriting the properties of blockchain: programmable, borderless, and settleable in seconds rather than days. USDT, issued by Tether, and USDC, issued by Circle, together represent the dominant share of the stablecoin market, which has grown substantially since 2021 as institutional adoption has accelerated. The blockchain payment rails beneath them are fast, cheap, and critically invisible to end users. This invisibility is not a limitation. It is the point.

Visa, PayPal, and the Race to Integrate Stablecoin Infrastructure

The companies moving fastest are not crypto-native startups. They are incumbents who understand that the value of a payments network lies in its distribution, not its underlying technology and who are using stablecoins to upgrade the infrastructure their existing customers already rely on.

Visa’s stablecoin settlement programme allows card issuers to settle transactions in USDC rather than in dollars, eliminating the multi-day delay of traditional bank clearing. The cost case is compelling: cross-border transfers typically cost between 3% and 7% of the transferred amount in combined fees, according to the World Bank’s 2024 Remittances Prices Worldwide report. Stablecoin settlement can reduce that cost by an order of magnitude.

PayPal’s PYUSD is a more direct integration. By issuing its own stablecoin, PayPal keeps settlement on its own rails, earns yield on the reserves backing the token, and gains a programmable asset it can deploy across its more than 400 million active accounts. From the perspective of most PayPal users, nothing has changed. That is precisely the strategic intent. Stripe’s 2024 re-entry into crypto through stablecoin payouts to merchants in more than 150 countries follows the same logic: blockchain as back-end, familiar interface as front-end.

The Payment Networks That Users Will Never See

The most consequential infrastructure changes are often the invisible ones. Consumers did not notice when SMS networks gave way to data-based messaging protocols, or when magnetic-strip cards were replaced by EMV chips. They noticed only that things worked differently and then they stopped noticing at all.

Stablecoin payment infrastructure is following the same trajectory. Stripe’s stablecoin merchant payouts look identical to a standard bank transfer from the recipient’s perspective. Visa’s USDC settlement is transparent to cardholders. PayPal’s PYUSD operates behind the same interface its users have always known. The companies that will define the next decade of payments are not the ones making announcements about blockchain adoption. They are the ones embedding stablecoin infrastructure so deeply into their existing products that their customers simply notice cheaper fees and faster settlements and never think to ask why.

What Stablecoin Adoption Means for the Next Decade

Two regulatory developments cleared the largest institutional obstacle. In the United States, the GENIUS Act advanced through the Senate in 2025, establishing the first federal framework specifically for stablecoin issuers, with requirements for 1:1 reserve backing and regular audits. In the European Union, the Markets in Crypto-Assets regulation brought stablecoin issuers under a harmonised licensing regime from mid-2024. Neither regulation stopped the technology. Both gave institutions the legal certainty they needed to build on it at scale.

The economic implications are substantial. Cross-border remittances cost an average of approximately 6.4% globally in 2024, according to the World Bank’s Remittances Prices Worldwide data. Stablecoin rails can reduce that cost by a factor that no incremental upgrade to SWIFT can match. Settlement cycles that currently run two to three business days through correspondent banking compress to minutes.

The irony is that crypto’s most vocal advocates spent years predicting that blockchain would disrupt banks through confrontation. The disruption is arriving instead through the most ordinary of mechanisms: faster settlement, lower costs, and infrastructure that works well enough that most people will never need to know what it runs on.